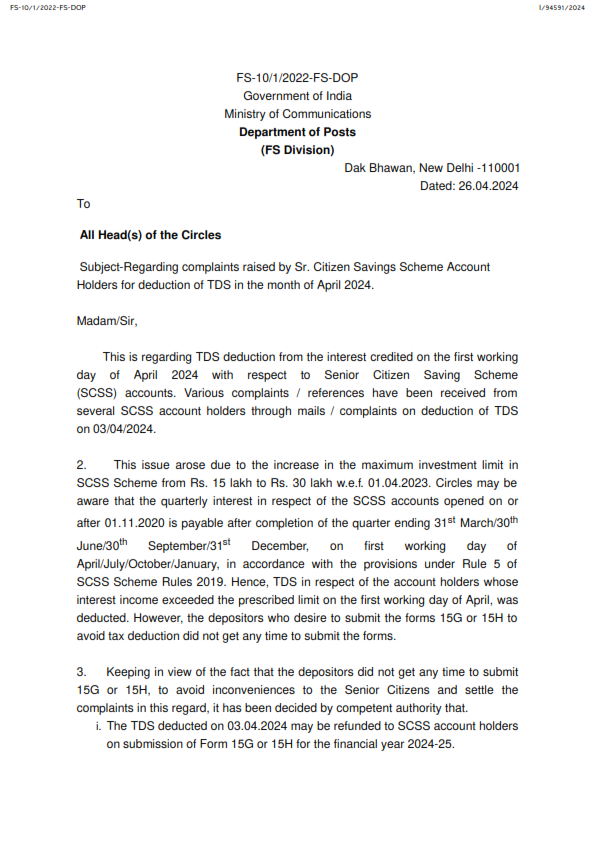

27/04/2024

Complaints raised by Sr. Citizen Savings Scheme Account Holders for deduction of TDS in the month of April 2024

26/04/2024